Commercial Mortgages Toronto & Ontario: AI-Powered Analysis for Multi-Unit, Development & High-Rise Projects

Financing commercial real estate and development projects in the GTA requires different expertise, lender relationships, and analysis than residential mortgages. Whether you are acquiring a stabilized 60-unit apartment building, developing a new high-rise mixed-use project, or refinancing an industrial portfolio, the underwriting focuses on cash flow, borrower track record, and project feasibility — not just personal income and credit.

At YourFinancing, we combine deep broker relationships across Schedule 1 banks, credit unions, life companies, CMHC, and private capital with tools that can assist in preparing analyses and packages. This can help support more efficient processes in many cases.

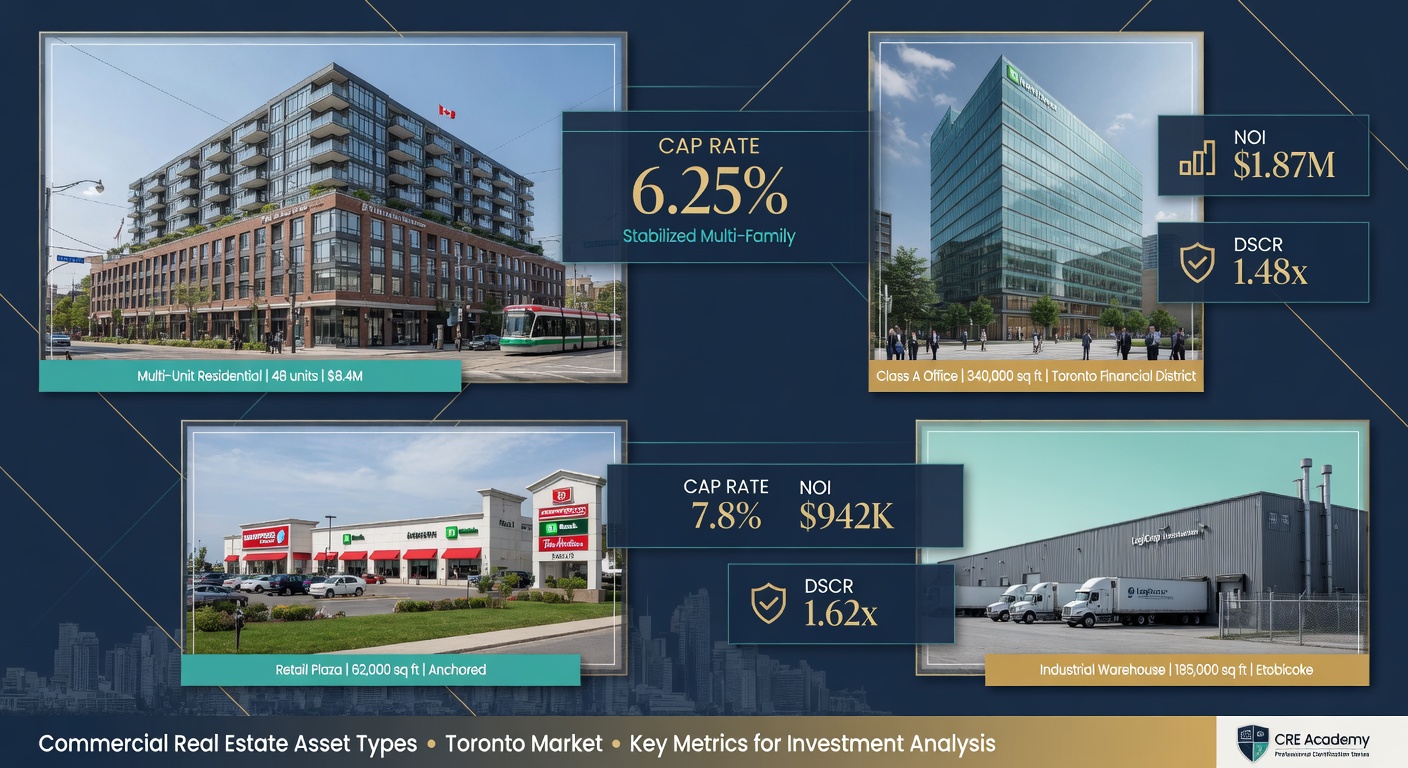

Types of Commercial Mortgages in Ontario

- Multi-Residential (5+ units): Purpose-built rental apartments, student housing, seniors residences. Often benefits from CMHC programs for lower rates and higher leverage when affordability and energy efficiency criteria are met.

- Mixed-Use: Ground-floor retail or office with residential above — common in Toronto intensification corridors.

- Office: Single-tenant or multi-tenant buildings. Post-pandemic flight-to-quality has made Class A and well-located assets easier to finance than older inventory.

- Retail & Plaza: Strip plazas, grocery-anchored centres, and street retail. Strong covenants and location drive terms.

- Industrial & Logistics: Warehouses, flex space, last-mile facilities. Strong demand and rent growth in the GTA have made this one of the most financeable asset classes.

- Land & Development: Raw land, infill sites, and pre-construction financing for high-rise, mid-rise, and townhouse projects.

- Special Purpose: Hotels, self-storage, medical offices, data centres, and other niche assets.

Commercial vs Residential Financing: The Real Differences

Commercial lending is fundamentally cash-flow and asset-based. Lenders care most about the property’s ability to service debt and the borrower’s ability to execute.

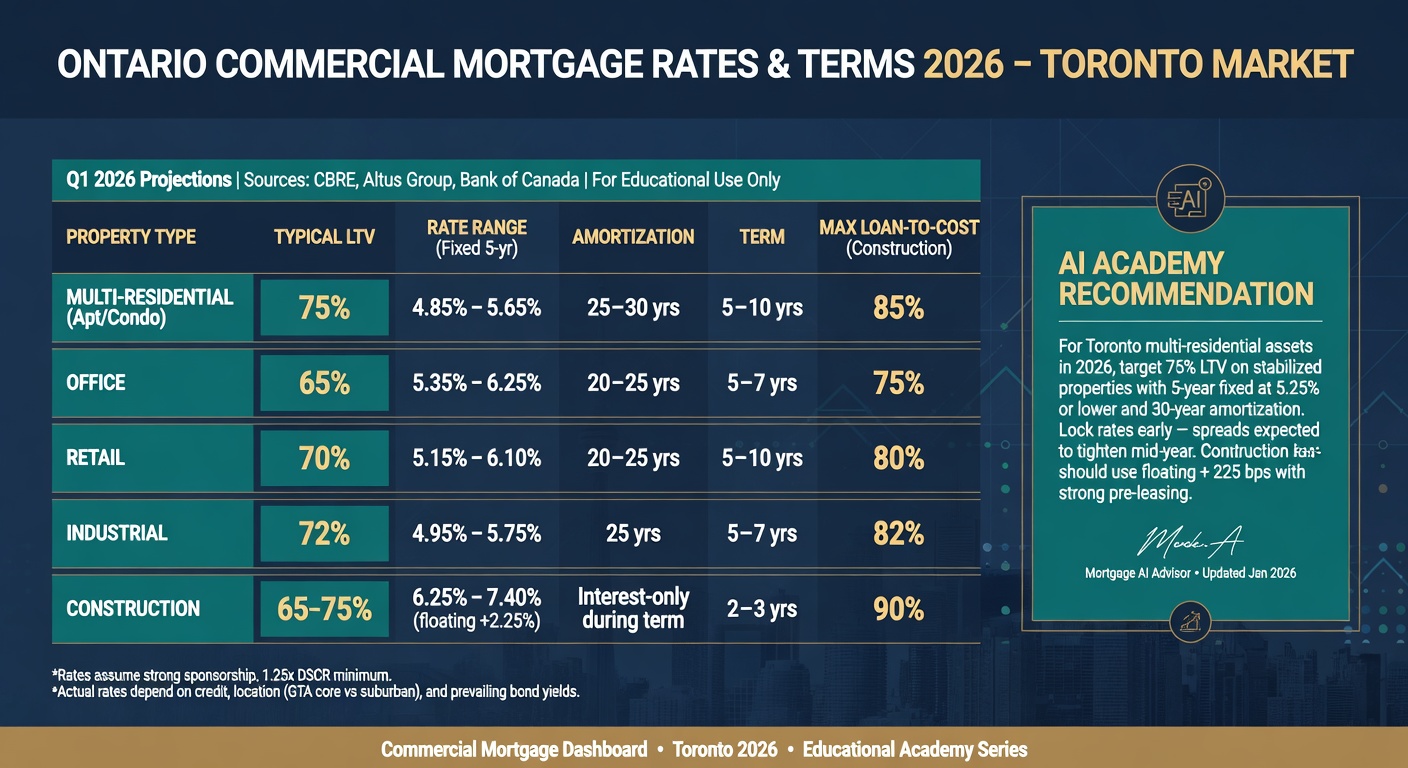

| Factor | Residential (1-4 units) | Commercial / Development |

|---|---|---|

| Qualifying Income | Personal income + rental (50-80%) | NOI, DSCR, borrower net worth & liquidity |

| Typical LTV / LTC | Up to 80% (insured) or 65-75% conventional | 60-75% on stabilized; 65-80% LTC on construction |

| Key Metric | GDS/TDS ratios + stress test | Debt Service Coverage Ratio (DSCR) 1.25x–1.50x+ |

| Amortization | 25–30 years | 20–25 years (interest-only periods common during lease-up or construction) |

| Recourse | Full personal guarantee usual | Limited recourse, carve-outs, or full recourse depending on sponsor strength |

| Documentation | T4s, NOAs, bank statements | Rent rolls, T12/T3 financials, leases, environmental, appraisals, engineering, pro forma |

| Timeline (traditional) | 1–4 weeks | 4–12+ weeks for complex development |

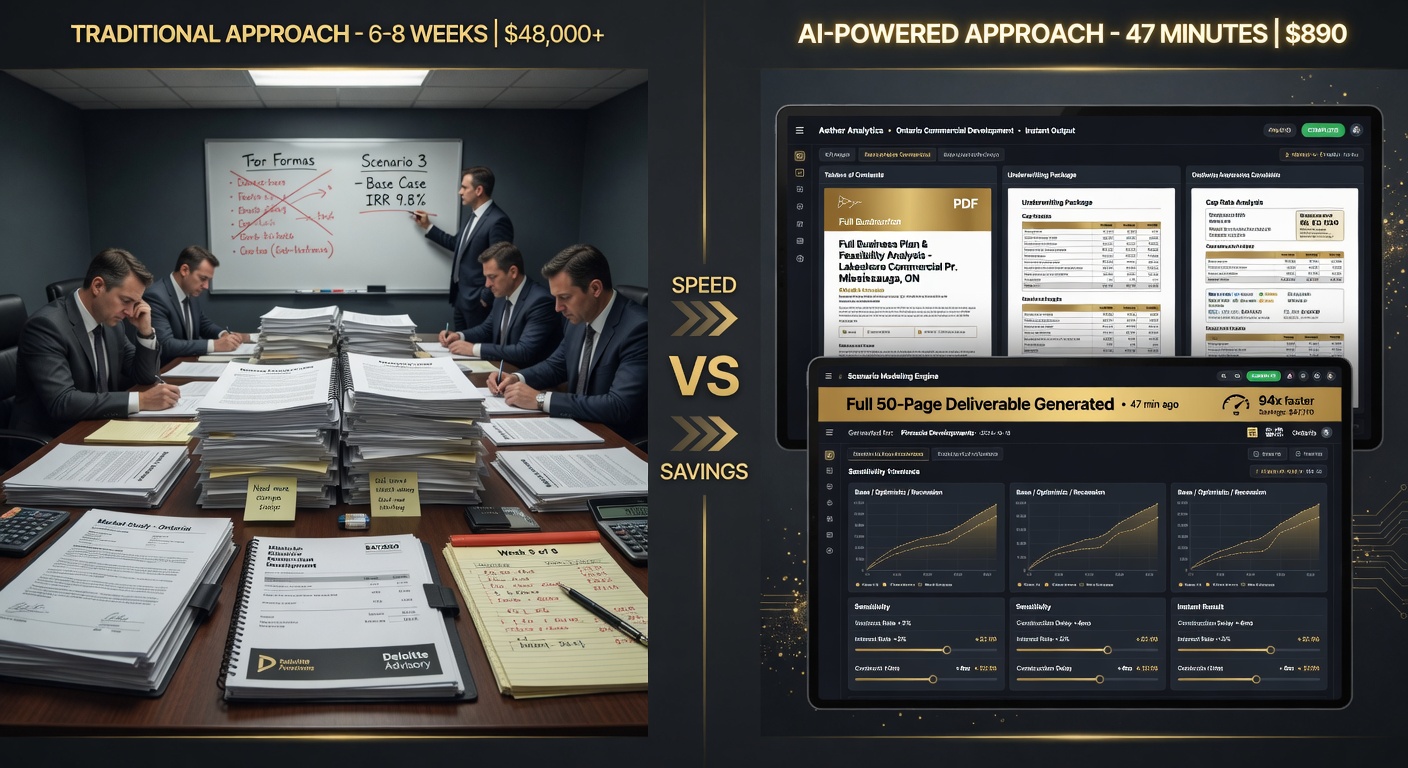

The AI Advantage: Full Business Plans, Feasibility & Analysis in Minutes — Not Weeks and Thousands of Dollars

Producing detailed lender-grade analysis for commercial projects can involve significant time and cost when using traditional methods.

Our platform changes the economics and the clock:

- Instant data ingestion: Upload rent rolls, T12 operating statements, development budgets, architectural plans, market comps, or even broker packages. AI extracts, normalizes, and cross-checks numbers in seconds.

- Automated pro forma & cash flow modeling: Generates base case, upside, and downside scenarios with correct accounting for vacancy, leasing commissions, tenant inducements, capital expenditures, and inflation assumptions appropriate to the asset class and submarket.

- Sensitivity & stress analysis: What happens if interest rates are 150 bps higher at take-out? Construction costs overrun by 18%? Absorption is 30% slower? AI runs dozens of scenarios in the time it takes to make coffee.

- Business plan / PIM drafting: Draft executive summary, investment thesis, risk factors, use of proceeds, and key assumptions in a format lenders and JV partners recognize.

- Lender-specific packaging: Different lenders emphasize different metrics (some love debt yield, others prefer stabilized DSCR at stress rate). AI re-optimizes the presentation for each target lender’s underwriting box.

- Preparation support: Tools can help accelerate initial analysis and documentation preparation compared to fully manual processes.

For a $25M high-rise development, every week of delay in securing committed financing can cost $40,000–$80,000+ in land carrying costs, consultant fees, and opportunity cost. AI-driven analysis doesn’t replace experienced commercial mortgage brokers or quantity surveyors — it removes the bottleneck so the right human experts can focus on structuring, relationships, and negotiation.

The combination of AI speed + broker judgment + established lender relationships is what allows us to deliver term sheets that are both competitive and achievable.

High-Rise & Large-Scale Development Financing in Toronto (Full Section)

Ground-up high-rise development (typically 10–50+ storeys) is one of the most complex and capital-intensive financing exercises in Canadian real estate. Lenders require deep due diligence on every aspect of the project: land cost and acquisition structure, zoning and approvals risk, construction budget and timeline, pre-sales or pre-leasing velocity, sponsor experience and liquidity, and exit strategy (take-out permanent loan or sale).

Typical Capital Stack & Financing Stages

- Land / Pre-Development Financing: Often 50–65% of land cost. Short-term (12–36 months), higher rates, strong emphasis on exit strategy and sponsor net worth. Environmental reports and planning status are critical.

- Construction Financing: 65–80% of hard + soft costs (Loan-to-Cost). Draw schedule tied to verified % complete (usually by independent quantity surveyor or architect). Interest reserve sized for the construction period plus lease-up. Cost overrun guarantees and performance bonds often required.

- Mezzanine / JV / Preferred Equity: Fills the gap between senior construction loan and sponsor equity. Higher cost, but allows sponsors to preserve liquidity or achieve higher leverage.

- Permanent / Take-Out Financing: Once stabilized (or for condo projects, upon substantial completion and registration), convert or refinance into long-term mortgage. For purpose-built rental high-rises, CMHC-insured programs can deliver very competitive rates and 30–40 year amortizations when criteria are met. Conventional life company or bank take-outs are also common for well-leased assets.

High-Rise Specific Considerations in the GTA (2026)

- Pre-Sales for Condo Projects: Most construction lenders require a minimum percentage of units under firm contract (often 60–80%+ depending on location and sponsor) before first advance. AI tools help model absorption curves and price elasticity under different market scenarios.

- Planning & Approval Risk: Toronto’s development approvals process (official plan amendments, zoning, site plan, Section 37/ affordable housing contributions, community benefits charges) can add significant time and cost. Lenders want clear paths and contingency for delays.

- Construction Cost Inflation & Supply Chain: Budgets must be stress-tested. Lenders increasingly require third-party cost validation and escalation allowances.

- Interest Rate & Take-Out Risk: Construction loans are usually floating. Sponsors and lenders model the rate environment at projected stabilization. Our rate forecast tools and scenario modeling are particularly valuable here.

- CMHC Multi-Unit Programs: For purpose-built rental (including high-rise), CMHC can insure loans at attractive rates with higher LTVs and longer amortizations when the project meets affordability, accessibility, and energy efficiency thresholds. The application and compliance process is rigorous — experienced brokers add real value.

- Environmental & Geotechnical: Phase I/II ESAs, soil reports, and remediation plans are almost always required on urban infill or former industrial sites.

Construction Loan Mechanics Most Borrowers Underestimate

Construction loans are not simple “pay interest only for two years.” Key details include:

- Advances are usually 80–90% of costs incurred to date (holdback on each draw).

- Independent cost-to-complete certification before each advance.

- Interest is often capitalized or paid from an interest reserve sized at stress rates.

- Change orders above a threshold typically require lender consent.

- Lease-up or sales velocity covenants must be met to avoid default or margin calls.

Our AI models these cash flow requirements dynamically so you see exactly when and how much equity you need to inject and when the project becomes self-funding.

Qualification & What Lenders Really Look For

Strong sponsors with proven track records in the same asset class and geography have a significant advantage. Lenders evaluate:

- Sponsor / Borrower: Net worth, liquidity (often 10–20%+ of project cost in liquid assets), experience (similar projects completed on time and on budget), and references.

- Property / Project Metrics: Stabilized NOI, current and projected DSCR at contract and stress rates, cap rate (implied and market), debt yield, break-even occupancy.

- Market & Location: Submarket fundamentals, comparable sales and leases, supply pipeline, demographic drivers.

- Reports: Current appraisal, Phase I ESA (and Phase II if flagged), engineering or building condition report, quantity surveyor review of construction budget for development deals.

AI helps surface gaps early (e.g., “your assumed 4% vacancy is optimistic for this submarket — here are the last 24 months of actual data”) so the package is realistic before it reaches the lender’s credit committee.

How the YourFinancing Commercial Process Works

- Initial Data Upload & AI Modeling — Share rent rolls, budgets, leases, site plans, or even a one-page project summary. We run base models and scenario analysis within hours.

- Broker Strategy Call — We review outputs, discuss capital structure options (senior + mezz, CMHC vs conventional, fixed vs floating), timing, and your priorities (speed, max proceeds, lowest cost, minimal recourse).

- Package Refinement & Lender Targeting — AI regenerates lender-specific versions. We approach the right 4–8 lenders (not shotgun 30) with warm introductions.

- Term Sheet & Due Diligence Coordination — We manage the back-and-forth, explain requirements, and keep the process moving.

- Closing & Ongoing — We coordinate with your lawyers, accountants, and project team. For development deals we often stay involved through draws and into take-out.

Representative Examples (Process-Focused)

These are illustrative of the type of work we do. Every deal is unique.

- 48-unit purpose-built rental acquisition in Etobicoke: AI stress-tested three different rate and vacancy scenarios and identified a CMHC-insured structure that improved DSCR by 0.18x versus the borrower’s original bank term sheet.

- 18-storey mixed-use development site in North York: Full construction-to-perm modeling (including interest reserve sizing and draw schedule) completed in under 48 hours. Allowed sponsor to negotiate tighter pricing with two competing lenders.

- Industrial portfolio refinance (three GTA assets): AI quickly benchmarked expenses against submarket norms and flagged two leases that were materially below market — strengthening the package and supporting higher proceeds.

Commercial and development lending involves material risks including interest rate volatility, construction cost overruns, leasing/absorption delays, environmental liabilities, and sponsor execution risk. AI tools improve information quality and speed but do not eliminate these risks or guarantee approval or terms. All financing decisions remain subject to full lender due diligence, credit committee approval, and market conditions at the time of commitment.

Next Steps

If you have a commercial acquisition, refinance, or development project in the GTA or broader Ontario, share high-level numbers and our team can work on preparing an initial analysis.

Quick Commercial DSCR & Loan Sizing Calculator

Rough order-of-magnitude tool only. Real underwriting uses full rent rolls, expense details, stress rates, and lender-specific boxes. For accurate modeling, use our full AI-assisted process.

Ontario cottage country or short-term rental properties? See dedicated pages: Cottage Financing and Airbnb & Short-Term Rental Financing.

This guide is for educational purposes. All financing is subject to lender approval, full due diligence, and current market conditions. Commercial lending terms, programs (including CMHC), and requirements change. Consult qualified legal, accounting, and tax professionals for your specific situation.