Mortgage Glossary & Encyclopedia for Ontario Buyers

Use this as your quick-reference mini-encyclopedia. Click any term or scroll through. All definitions are written specifically for the Toronto and Ontario market.

A–C

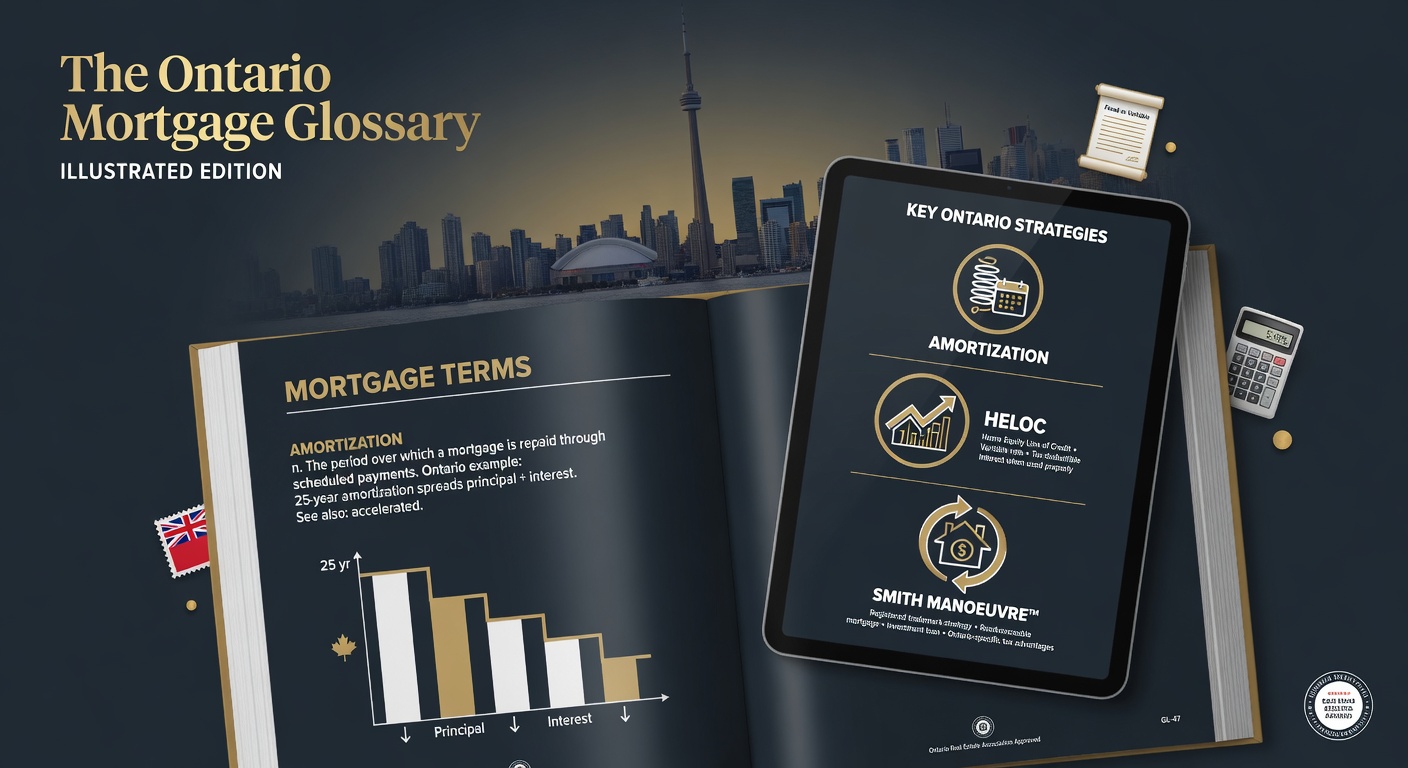

Amortization Period — The total length of time it will take to pay off your mortgage if you make only the scheduled payments. Common terms are 25 or 30 years. Shorter = less interest paid overall.

Appraisal — A professional estimate of your home’s current market value, usually required by the lender.

Bi-Weekly / Accelerated Bi-Weekly — Paying half your monthly payment every two weeks. Accelerated versions effectively add one extra payment per year.

CMHC Insurance — Mortgage default insurance required when you put down less than 20%. Protects the lender, not you. Premiums are added to your mortgage or paid upfront.

Conventional Mortgage — A mortgage with 20% or more down payment (no CMHC insurance required).

D–H

Debt Service Ratios (GDS / TDS) — Gross Debt Service and Total Debt Service. Lenders use these to decide how much you can borrow.

HELOC (Home Equity Line of Credit) — A revolving credit line secured by the equity in your home. You pay interest only on what you use.

High-Ratio Mortgage — Mortgage with less than 20% down (requires CMHC or similar insurance).

I–P

Interest-Only Mortgage — You pay only the interest for a period of time (principal stays the same). Rare in Canada for residential mortgages.

Lump Sum / Prepayment Privilege — The amount you can pay extra each year without penalty (often 15–20% of original principal).

Monoline Lender — Lenders that only do mortgages (not full-service banks). Often offer better rates through brokers.

Pre-Approval — A conditional commitment from a lender (or broker) stating how much they will lend you and at what rate, subject to final conditions.

Prime Rate — The benchmark rate set by banks. Most variable mortgages and HELOCs are quoted as Prime +/- a percentage.

R–S

Readvanceable Mortgage — A mortgage that automatically increases your available credit as you pay down the principal (very useful for Smith Manoeuvre).

Refinance — Replacing your current mortgage with a new one, usually to get a better rate, change terms, or access equity.

Renewal — When your current mortgage term ends and you negotiate new terms (rate, amortization, etc.) with your existing or a new lender.

Smith Manoeuvre — A strategy where you use a HELOC to borrow against home equity and invest the funds, making the interest tax-deductible while using investment returns to pay down the original mortgage faster.

Stress Test — The requirement to qualify at a higher rate (contract rate + 2% or the qualifying rate, whichever is higher). Designed to ensure you can afford payments if rates rise.

T–Z

Term — The length of time your current mortgage rate and conditions are locked in (usually 1–10 years). At the end of the term you must renew or refinance.

Title Insurance — Insurance that protects against title defects, fraud, or errors in the legal ownership of the property.

Variable Rate Mortgage — Rate fluctuates with the lender’s prime rate. Payments may stay the same or change depending on the product.

This is an educational reference only. Rules and products change. Always verify current details with a licensed mortgage professional.