The Smith Manoeuvre: An Educational Overview for Ontario Homeowners

The Smith Manoeuvre is a strategy that some Canadian homeowners consider. It involves using a HELOC to invest and potentially making interest tax-deductible under certain CRA rules, while using investment returns to pay down the original mortgage. It carries significant risks and is not suitable for everyone.

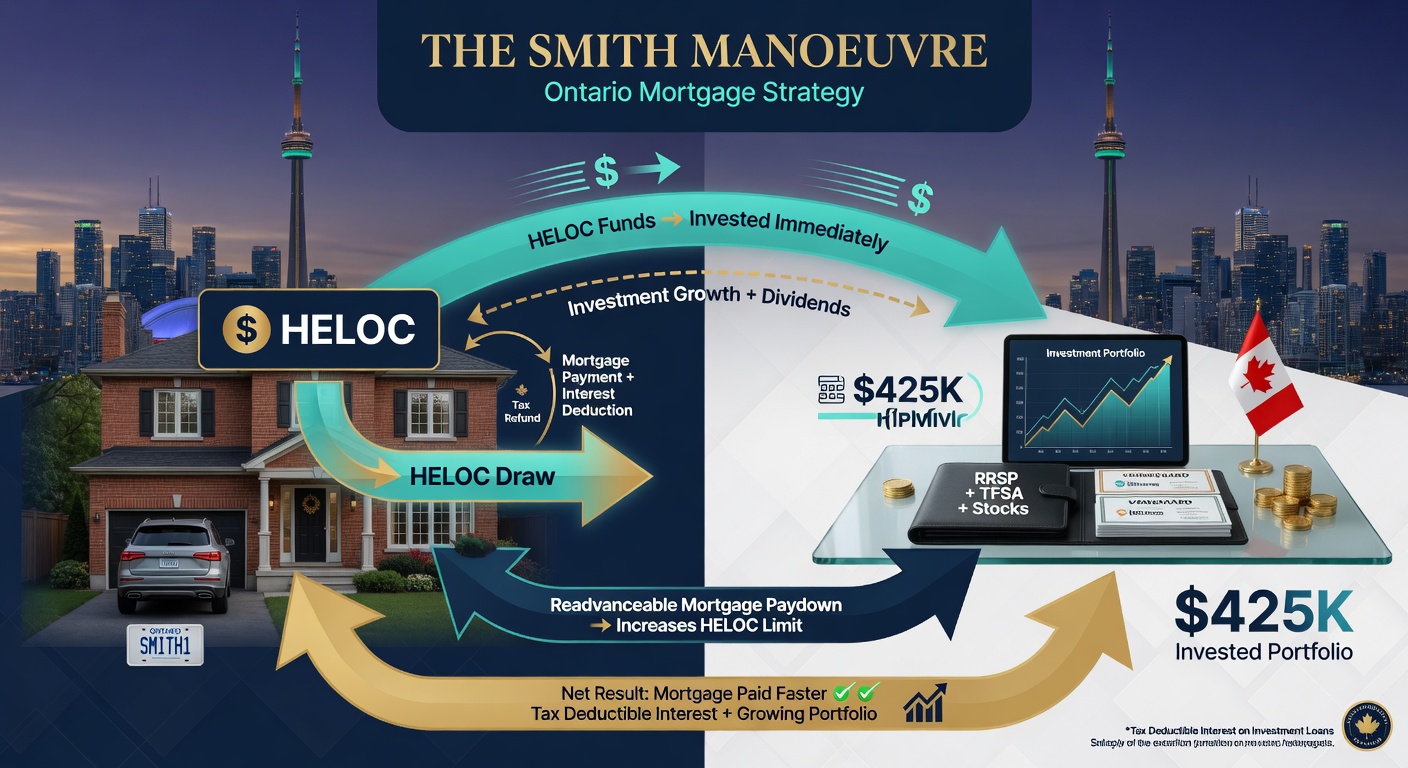

What Is the Smith Manoeuvre?

In simple terms: You borrow against the equity in your home using a HELOC (Home Equity Line of Credit) and invest that money in income-producing assets (stocks, ETFs, rental property, etc.). The interest on the investment loan becomes tax-deductible under CRA rules, while the money you earn from investments can be used to pay down your original (non-deductible) mortgage faster.

How the Smith Manoeuvre Works Step by Step (Ontario 2026)

- Get a readvanceable mortgage or HELOC — Many lenders in Toronto offer products designed for this strategy (readvanceable mortgages re-advance principal as you pay it down).

- Borrow against equity — As you pay down your mortgage, you borrow the same amount via HELOC and invest it.

- Invest the borrowed funds — Put the money into a non-registered investment account earning dividends, interest, or capital gains.

- Claim the interest deduction — The interest paid on the HELOC (investment loan) is tax-deductible. Keep excellent records.

- Use investment income + tax refunds to make extra payments on your original mortgage.

- Repeat — Over time your mortgage shrinks while your investment portfolio grows, and you get annual tax relief.

Realistic Example (Toronto Homeowner)

$800,000 home, $500,000 mortgage at 4.5%, 25-year amortization.

After 5 years of normal payments you’ve paid down ~$70,000 in principal.

With Smith Manoeuvre: You borrow that $70k via HELOC and invest it.

Assume 7% average annual return on investments and 40% marginal tax rate.

Annual interest deduction ≈ $3,150 (at 4.5%). Tax savings ≈ $1,260/year.

Over 10–15 years the compounding + tax savings + accelerated mortgage payoff can be worth well over $100,000 in net benefit (before risk is considered).

• This is not “free money.” You are increasing leverage and taking market risk.

• Investments must be income-producing (CRA will challenge personal-use or speculative investments).

• Interest rates on HELOCs are usually variable and higher than fixed mortgage rates.

• If the market drops, you could owe more than your investments are worth.

• Proper documentation is critical. Many people get this wrong and lose the deduction.

Who the Smith Manoeuvre Makes Sense For

- Homeowners with significant equity (usually 20–30%+)

- Those in higher tax brackets (30%+ marginal rate)

- People with stable income and high risk tolerance

- Those who plan to stay in the home long-term (10+ years)

How a Mortgage Broker + AI Helps with the Smith Manoeuvre

Not every lender or mortgage product works well with this strategy. A knowledgeable broker can:

- Find readvanceable mortgages and competitive HELOCs

- Structure the borrowing correctly from day one (very important for CRA)

- Coordinate with your accountant or financial advisor

- Run scenarios showing realistic net savings vs risk

Next Step

If you have substantial home equity and are interested in advanced strategies like the Smith Manoeuvre, book a conversation with our team. We can model it specifically for your numbers and current mortgage.